Two Standard Deviations

Outliers will happen

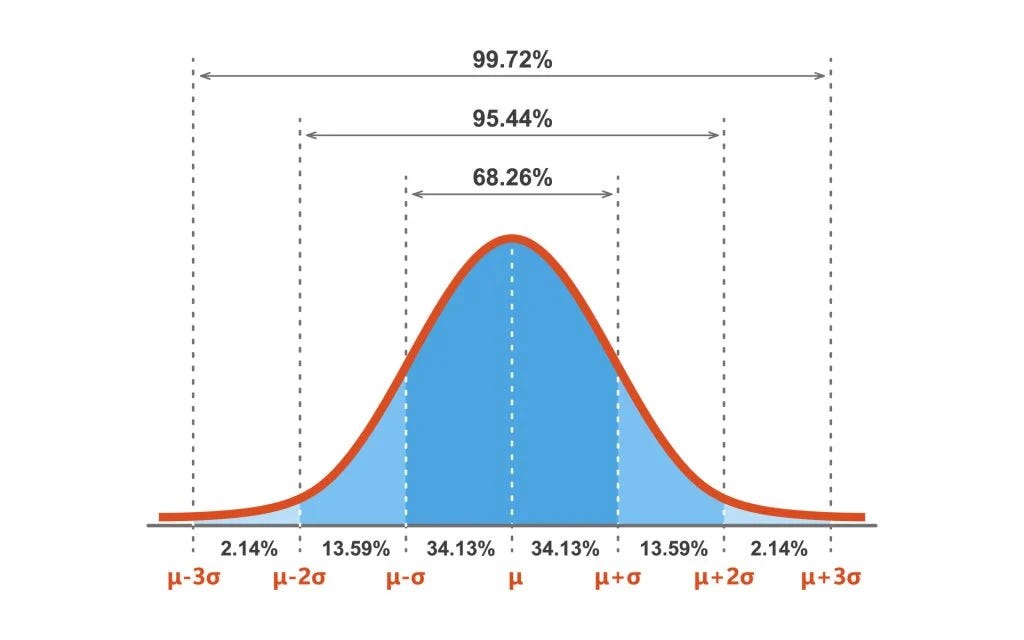

In a normal bell curve (which admittedly doesn’t really describe financial markets but is reasonably close and makes the math much easier,) a little more than 2% of the time, you’re going to get a surprisingly bad result, even with a strategy that works over time. Considering roughly 252 trading days in the year, that means five days out of the year, you’re likely to do surprisingly poorly.

Why do I bring that up? On Friday, while the market was driven higher by large cap tech, the Russell 2000 was flat, and our stocks also did poorly. Yes, I could just ignore that and hope nobody noticed, but I tend to write about what I’d want to know about, and nobody ever called me a clever marketer. So, what happened and is it a problem?

I don’t think Friday represents a problem and if it was, I’d do something about it. If our stocks violate what we expect of them, they get sold. If we no longer believe a stock can contribute to the portfolio, we sell them. That’s life. I bring up standard deviation because sometimes you just get unlucky. Imagine taking a six-sided die and rolling a 1 twice in a row. That’s unlucky, but only a fraction of a percent more frequent than a two standard deviation event.

In this case, we happened to have some bad news all happen on the same day. For instance, ASTS just closed a convertible bond, where many short stock against it to hedge out the equity risk. This is at the same time as a lot of space plays are also struggling, with liquidity and inflation risks recently present, hurting high beta and momentum stocks. I worry about every stock we own, that’s part of my job, but I like my odds here. Board members have bought on the open market at these levels and institutional investors are buying. They’ve shown the product works and the satellite launches should increase in pace.

We also had another round of software fear on Friday, with Anthropic announcing a code security AI app that hit cybersecurity stocks. That hit FTNT for -2% and put the chill on other software names. I won’t rehash the software debate here; I’ll just note software overall has failed to hit new lows. This news caused selling and hurt our Friday but not to a level worse than we’ve seen in the recent past.

Another problem was in chemicals, with Chemours (CC) reporting soft earnings on bad industrial business, which in turn sent our DOW stock -3%. The thing is, there isn’t much overlap between the companies. CC is about high-value, complex chemicals, while DOW is about plastics and commodities. There’s just not much overlap and thus, not much reason DOW should get sold.

I don’t want to go into exhaustive detail, here, I just want to point out that sometimes a surprisingly good mix of events come about and sometimes you get a bad mix. On Friday, we got the bad mix. It happens. Fortunately, sometimes, you should also have good days, and we got some of those to start the year. That helps a lot.

You can’t change the past, but you can monitor the likelihood the bad times continue. In this case, I think we have cause for cheer. The SOFR-IORB spread had been climbing, indicating pretty fundamental funding stress, but that started to reverse on Friday. Credit spreads had also been climbing until reversing on Friday. While PCE was a bit hot, Treasury bond inflation expectations improved, a bit. Fundamentally, the macro environment remains good.

Bad days will happen, if only from basic randomness. While we try to control for that, making long-term gains is more of a core focus for us. There will be further risk events, such as NVDA earnings on Wednesday. Those risk events have been amply hedged by the market, with shorting high. I continue to like the odds of being optimistic, here, as nothing yet has seemed to break enough to cause prolonged trouble. If shorts don’t payout soon, buying pressure is likely to appear.